Mutual Funds vs ETFs

Exchange-Traded Funds (ETFs) were first introduced in the early ‘90s with the launch of the SPDR S&P 500 Trust (ticker: SPY) by State Street Global Advisors. Over the last 30+ years, ETFs have experienced widespread adoption with investors and rapid asset growth. Much of this growth came at the expense of traditional mutual funds. With billions of dollars in investable assets at stake as well as the fees those dollars generate, the Wall Street marketing machine has been working overtime espousing the benefits of ETFs compared to traditional mutual funds. But is the ETF structure truly superior?

Like most things in life, the answer is much more nuanced, with distinct advantages and disadvantages for both mutual funds and ETFs. We believe investors can be well served using either structure; however, compared to mutual funds that are already managed in a low-cost, tax-efficient manner, there may or may not be benefits to using ETFs.

Before we dive into analyzing these two investment vehicles, a little background may be helpful.

In simple terms, both mutual funds and ETFs are structures used to hold portfolios of stocks, bonds, or a combination of both. ETFs trade on an exchange like stocks, while mutual funds trade directly with the fund provider. Both structures can give investors an efficient and low-cost way to access capital market returns.

To help clarify the major differences between the two structures, we will look at three relevant variables:

- Commissions/Premium Discounts (Trading Costs)

- Operating Expenses

- Tax Efficiency

Commissions

Most investors are familiar with commissions, so we will start the analysis here. Commissions are simply a fee paid to buy or sell a fund. Although commissions vary by custodian, we will limit our analysis to variables that our clients are exposed to.

Trading commissions have been under pressure for many years. ETFs now trade commission-free, while some, but not all, mutual funds trade with a small fee (average $10-15). Although zero is certainly better than $10-15, this benefit is usually not material, particularly for long-term focused investment portfolios with relatively low turnover in funds. It is also important to note mutual fund commissions may be pushed to zero just like ETFs. While this very slight benefit currently favors the ETF structure, it is neither material nor likely to be persistent.

Commissions are not the only trading costs that need to be considered. Unlike mutual funds, which trade at their net asset value (NAV) directly with the fund provider, ETFs trade on an exchange at the bid/ask prices.

The difference between the bid price and the ask price is referred to as the spread. The “bid” is the price the dealer is willing to pay for the ETF. The “ask” refers to the price at which the dealer is willing to sell the ETF, which is slightly higher. As a result, the investor will typically buy ETFs for slightly over market price and sell for slightly under market price.

Spreads change daily and can be immaterial for some ETFs while markedly material for others. Regardless of its size, the spread is a cost associated with trading ETFs.

Premiums/Discounts

In addition to the spread, ETF buyers and sellers need to be aware of the fund’s premium and discount. As the name implies, a premium exists when the ETF’s price is more than the fund’s NAV or the value of its underlying securities. A discount exists when the ETF’s price is less than the NAV. Depending on which side of the transaction you are on, a premium or discount can help or hurt.

Premiums and discounts need to be monitored, as they change daily and can be volatile, particularly during risky markets. For example, during “peak COVID” in early 2020, many fixed-income ETFs traded at a material discount to their NAV. Great (in hindsight) if you were a buyer. Not so great if you were a seller.

ETF investors must be aware of the premium and discount when trading, as they present yet another cost to consider. Since mutual funds are traded at a single NAV at the end of the day, there is no need to worry about any premium or discount.

ETF investors must be aware of the premium and discount when trading, as they present yet another cost to consider. Since mutual funds are traded at a single NAV at the end of the day, there is no need to worry about any premium or discount.

Operating Expenses

In addition to spreads and premiums/discounts, investors should be aware of a fund’s operating expenses. The operating expense is simply what the fund company (sponsor) charges to create and manage the fund. It is a fee paid directly from the fund’s assets or, more correctly stated, your assets.

Two decades ago, ETFs gained popularity by providing considerably lower expenses in comparison to the prevailing fees of mutual funds. As the relationship between fees and performance became well understood, investors flocked to the lower-cost ETF structure, causing its assets to drastically increase, usually at the expense of assets that otherwise would have been placed in a mutual fund. To slow these outflows, mutual fund providers had no choice but to follow suit and lower their fees – it was pure capitalism at work.

Tax Efficiency

Due to their structure, most ETFs will not make annual capital gain distributions, minimizing potential year-end liabilities. The mechanics behind how ETFs do this (the in-kind creation/redemption process) is beyond the scope of this article. Unfortunately, like trading costs, this unique benefit could be over-simplified.

First, the tax efficiency of any strategy will be strongly related to its investment approach. Low turnover and broadly diversified strategies inherently lend themselves to tax efficiency. Until the SEC adopted the ETF rule in 2019, virtually all ETFs were tax-efficient index strategies, giving them a natural advantage over their actively managed, higher-turnover mutual fund peers. This helped set in motion the dogmatic belief that ETFs are materially more tax efficient. Regardless, extremely tax-efficient mutual funds can be found today. As the distributions of ETFs decrease in size, the tax-advantaged structure of these funds will become increasingly marginalized. It is similar to two cars driving on a highway, one at 55 miles per hour and the other at 56. You’re going to arrive at the same place at virtually the same time.

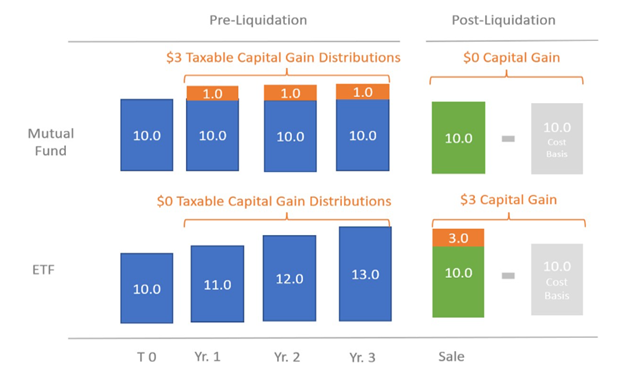

Second, ETFs allow for tax deferral, not tax avoidance as some investors believe. The graph below outlines how ETFs and mutual funds differ in their treatment of capital gain distributions.

Source: Savant Wealth, for illustration purposes only

Assume the two funds represented above are identical in every way with the exception of their structure – one is a mutual fund, the other an ETF. Both have a starting NAV of $10.00 and the same $1.00 per year appreciation. In the event that a mutual fund distributes all of its gains each year, there will be no gains to acknowledge at the point of sale. The ETF, which distributes none of its gains, will cause the investor to realize all of the capital gains at the time of sale, as its undistributed gain will increase the fund’s NAV.

According to KPMG, “The deferral of gains at the ETF level using in-kind redemptions for appreciated securities generally doesn’t alter the total amount of taxable gain to be realized when the shareholder ultimately sells or redeems his or her ETF shares.”1

The ETF’s tax deferral does have some additional benefits, such as the ability to control when that liability is created (at the sale) and the growth of the avoided tax liability. That benefit, however, may be marginalized relative to a mutual fund that also pays little to no capital gains.

Conclusion

Capital markets are always innovating and changing, as new products are introduced daily. Today, there are more mutual funds (7,4812) and ETFs (2,6322) available than there are publicly traded stocks (6,203 on the NYSE and Nasdaq3). With so many offerings, investors can find extremely competitive, low-cost, tax-efficient funds in either structure.

In addition to structure, there are other important factors to consider when managing an investment portfolio. First and foremost are the selection and sizing of asset classes and the underlying investment strategies that are inside the ETF and mutual fund structures. Beyond that are other activities that can make a difference in cost and tax efficiency, such as tax engineering assets in various account types (taxable, tax-deferred, and after-tax) as well as tax-loss harvesting.

1KPMG ETF Tax Efficiency Fact or Fiction?

2As of 12/31/2021, Investment Company Institute (ICI) 2022 Investment Company Fact Book

3As of 5/6/2022, World Federation of Exchanges (WFE) 2021 Annual Statistics Guide